Despite signs of stabilisation since H2 of 2017 the ICT sector remains fragile, with businesses’ profit margins expected to shrink further in 2018.

- The ICT value chain in the UAE encompasses vendors, distributors, power retailers, resellers and other small retailers, while manufacturing is not present. Most of the vendors and distributors are present in Dubai’s free trade zones and redistribute to the wider Middle East.

- Despite the crude oil price rebound in 2018, downward pressure on the economy and discretionary spending, including the ICT segment, continues to persist. According to BMI Research, ICT spending in the Middle East is estimated at USD 235 billion in 2018, which is just a slight increase compared to 2017.

- The UAE’s ICT market remains characterised by high competition, single-digit margins, low entry barriers, lack of support from banks and stagnating growth in subsegments like PCs and desktops. The imposition of new taxtion and customs duties on certain consumer durables and IT products sold in India and persistent political instabilitiy in the Middle East region has negatively impacted the overall demand of ICT products.

- Payment delays and protracted defaults have sharply increased since 2015, as have run-away cases, which become increasingly more frequent due to cash problems in this industry. Although we have seen some signs of stabilisation since the second half of 2017, the sector remains fragile and volatile, with businesses’ profit margins expected to shrink further in 2018. One of the main reasons for the increased default rate remains the lack of support from banks in the form of reduced or cautious lending. The payment delays and insolvency outlook remains subdued in 2018.

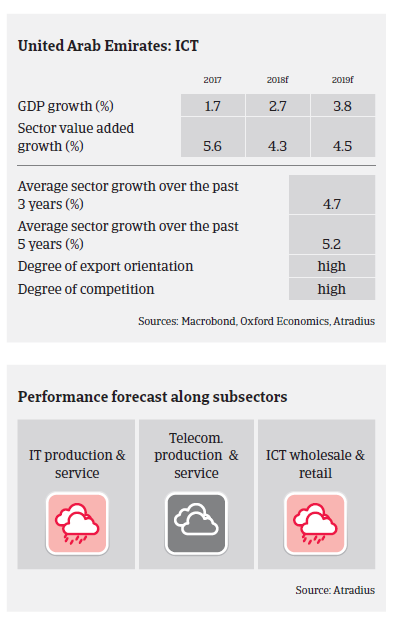

- We continue to adopt a prudent and selective approach on buyers in the ICT sector in UAE, especially for the wholesalers and retail segment, which has severely suffered from lower demand, high competition and deteriorated margins. Special attention is also given to distributors and resellers exporting to high political risk countries in the Middle East and Africa. In the telecommunication sector we maintain a prudent approach with smaller players. In any case, the availibility of the latest audited financials and updated trading experience are key requirements for business reviews in the ICT sector.

Related documents

Market Monitor ICT June 2018

1.04MB PDF