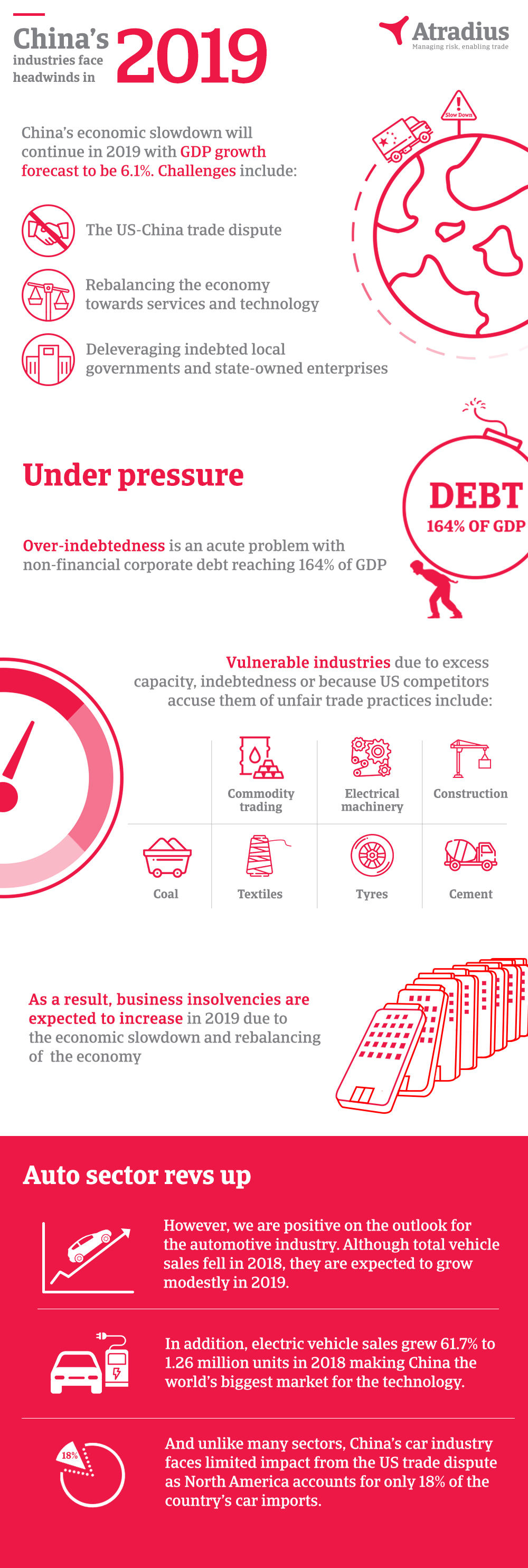

From navigating trade talks with the US to deleveraging indebted state-owned enterprises, China faces a number of downside risks in 2019.

For that reason, at Atradius we expect the economic slowdown to continue this year with GDP growth forecast to reach 6.1%, according to Oxford Economics.

The US-China trade talks are one of the biggest headwinds facing the Chinese economy. While it is positive that China and the US have continued trade negotiations past the 1st March deadline for introducing new tariffs, it remains uncertain whether the talks will lead to an agreement. And even if an agreement is made, China’s structural economic conflict with the US will remain unresolved.

In light of the risks, Beijing has taken measures to support the economy that include boosting liquidity and increasing infrastructure investment. However, the Chinese economy also faces domestic structural issues that will continue to dampen economic growth over the next few years. These include the need to deleverage local government and corporate balance sheets, and rebalancing the economy towards services and technology.

{kind=link}

Debt burden

The indebtedness of Chinese industry is a particularly acute problem with non-financial corporate debt reaching 164% of GDP. While progress has been made to rein in credit growth, business insolvencies in China are expected to increase further in 2019.

Vulnerable sectors include highly indebted companies in industries with overcapacity such as aluminium, cement, coal, commodity trading, construction, and steel and metals. In addition, the ongoing uncertainty over the direction of the US trade policy means Chinese businesses dependent on sales to America are at risk. This is especially true for companies that US competitors have accused of unfair trade practices in sectors such as metals, electrical machinery/electronics, textiles and tyres.

In the driving seat

One sector our experts are positive on is the automotive market. Although total vehicle sales in 2018 fell by 2.8% year-on-year to 28.1 million units, commercial vehicle sales showed a healthy expansion, growing by 5.1% year-on-year to 4.4 million units. Moreover, total vehicle sales growth is estimated to be flat or positive in 2019, showing that the decline has stabilised for now.

And unlike many sectors, China’s car industry faces limited impact from the US trade dispute as imports and exports account for a tiny share of domestic production, and of the imports, North America makes up only 18%.

Fully charged

A bright spot are electric vehicles for which China is the biggest market in the world. Sales grew a whopping 61.7% to 1.26 million units in 2018 with pure electric vehicles up 50.8% to a record 984,000. While they remain a small proportion of China’s overall car market, electric vehicle sales will continue to grow strongly thanks to supportive government policies that include providing incentives to carmakers and subsidies to consumers, enhancing charging facilities across the country, and allowing buyers to be exempt from the licence-plate lotteries that determine who can buy a car.

Despite the positive outlook, the electric vehicle market faces some downside risks. Overcapacity is one issue given the industry’s potential to produce 20 million units even though the current government plan is to have only seven million units on the road by 2025. In addition, competition is set to pick up when China lifts a cap restricting foreign ownership of car companies by 2022.

In the more immediate future, Chinese companies have to contend with challenges such as uncertainty over trade negotiations, slowing economic growth and high levels of corporate debt.

Through our strategic presence in over 50 countries as well as access to credit information on millions of companies worldwide, Atradius aims to help you confidently navigate the credit risks that are an intrinsic part of global trade, and successfully conduct business in the world's second-largest economy.

Related documents

8.32MB PDF