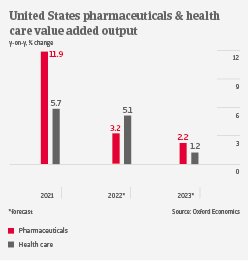

Robust growth expected in 2022

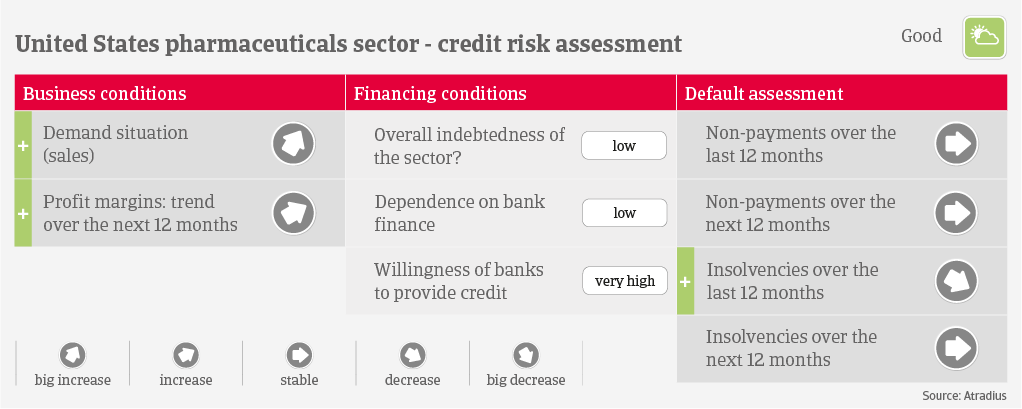

The US accounts for about 45% of the global pharmaceutical market and 22% of global production. US pharmaceuticals output and sales remain robust in 2022, driven by the ongoing global vaccination rollout and pent-up demand for essential and non-essential medical treatments. Margins of brand name drug producers have soared in 2021, resulting in strong cash flow. However, wholesalers/ distributors still trade on thin margins, despite growing sales. Some of them still have payments to make in connection with opioid-related lawsuits and litigations.

While sector growth in 2022 and 2023 will be mainly driven by vaccinations, the ageing population will spur drug demand in the mid- and long-term. The decision of the Supreme Court to uphold the Affordable Care Act (Obamacare) also supports future growth prospects of the industry. However, pressure from legislature to reduce healthcare costs could rise again once the pandemic ends. This could affect investments, given the high R&D costs for producers.

Several pharmaceutical producers and distributors have taken advantage of historically low lending rates in order to pursue debt-financed acquisitions. Most of them used their strong cash flow to deleverage after larger takeovers, thereby maintaining their credit ratings. Payment duration in the industry can vary between 30 and 150 days. Major drug producers often use their leverage against suppliers to achieve longer payment terms and build cash flow. While non-payments are generally low in the industry, non-payment notifications have increased in the segment of small community-based pharmacies. Those businesses often compete against larger chains and face reimbursement pressures from public payers (e.g. Medicaid and Medicare).

Due to a government crackdown on opioids, a number of producers, distributors, and pharmacies heavily exposed to sales of such drugs were forced to close their businesses and/or file for bankruptcy between 2017 and 2020. Since then, business failures have returned to a very low level. Our underwriting stance is open for drug producers and distributors, while we are restrictive for small pharmacies due to increased payment delays.

Related documents

969.0KB PDF