Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights

Singapore

Singapore

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Singapore

Romania

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United Kingdom

United States

United States

Survey findings in India set the backdrop for a business environment where payment behaviour and corporate liquidity is under pressure. Within this context, around half of B2B sales are conducted on credit, a share above the regional average and among the highest in Asia. This places India alongside more developed trade credit markets such as Singapore and closer to Vietnam than most of its regional peers. The recent expansion in credit use has also been stronger than across Asia, driven primarily by large industrial firms. This reflects both competitive pressures and the need to sustain commercial activity in a more demanding operating environment.

Payment terms typically extend from one to two months from invoicing, longer than in most Asian markets. This structurally lengthens the payment cycle and increases exposure to delays. At the same time, B2B payment behaviour remains less stable than across the region, pointing to a more volatile and less predictable environment. Although occasional improvements in payment performance are reported more often than deterioration, delays remain widespread. Nearly nine in ten firms report overdue invoices, with outstanding payments accounting for more than one third of receivables, above the regional average.

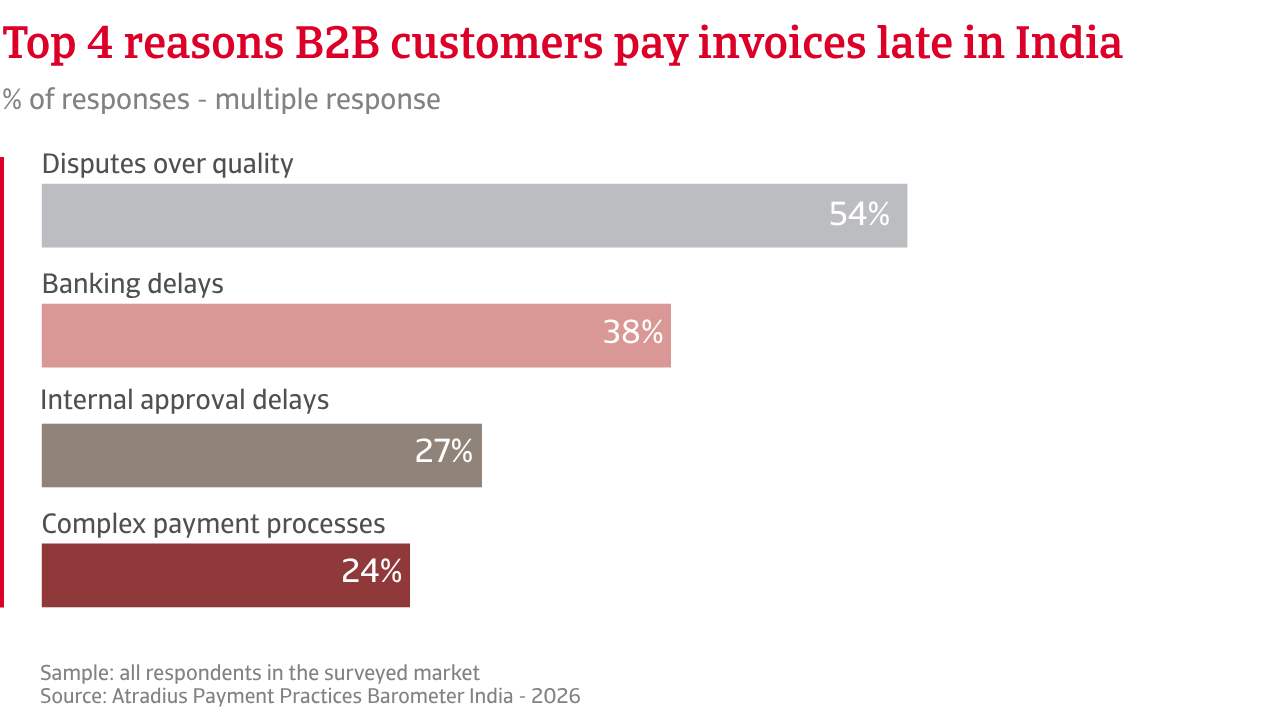

The drivers of these delays highlight underlying financial strain. Indian firms are more likely than their regional peers to cite customer liquidity constraints as a cause of late payment. Operational frictions, including approval and banking delays, also play a more prominent role. Together, these factors create a risk environment that combines financial pressure with process inefficiencies, increasing the need for close monitoring and effective cash flow management.

Despite relatively long payment terms, the overall collection cycle remains efficient compared to the regional average, as shown by Days Sales Outstanding (DSO), which also highlights a significant share of payments remaining long-term overdue. Progress in reducing this exposure has been limited in recent months, and long-term delays continue to increase the likelihood of losses.

This is reflected in the bad debt profile. More firms report rising write-offs than declines in recent months, in line with Asia but affecting a larger share of businesses in India. Losses above 5% of receivables are more common, placing additional pressure on cash flow and margins. Write-offs in India are frequently linked to unresponsive customers rather than formal insolvency, making recovery more difficult. This points to a more complex and less structured credit environment.

The impact on working capital is clear. Payment risk disrupts cash flow planning and increases reliance on external financing. Rather than being fully absorbed, this pressure often passes through the supply chain, as firms delay payments to suppliers. As a result, financial flexibility is reduced, leaving businesses with fewer internal buffers to manage operational liquidity needs.

In response, firms in India adopt a more active approach to risk management. They rely less on provisions and more on operational tools, including tighter payment terms, advance payments and closer credit control. Digital tools and customer diversification support faster intervention, while the use of credit insurance is more widespread, particularly among smaller firms in industry. This reflects a need to protect cash flow in a less predictable payment environment, amid uncertainty around economic conditions, global trade flows, and geopolitical developments impacting business operations.

Around half of B2B sales are conducted on credit, a share above the regional average and among the highest in Asia. This places India alongside more developed trade credit markets such as Singapore and closer to Vietnam than most of its regional peers.

Even as current data signals, continued pressure on collection cycles and bad debt exposure, Indian firms, particularly mid-sized businesses and those in industry, remain more optimistic than their Asian peers about the outlook for B2B payment behaviour in the coming months. This suggests companies are tightening controls and managing customer risk more actively, with early signs of improvement reflected more in expectations than in current outcomes.

Consistent with this environment, many firms in India still struggle to clearly assess the direction of change. Nearly half expect insolvencies to remain elevated, in line with the regional share, pointing to ongoing stress in the business landscape. At the same time, fewer firms anticipate a further rise in insolvencies compared with Asia, suggesting more cautious expectations. A relatively larger share of businesses also report uncertainty, highlighting limited visibility on how conditions may evolve in the near term.

Expectations of improved profitability in the months ahead remain widespread. However, this sits alongside persistent pressure from delayed payments, liquidity constraints, and rising bad debt. The contrast points to a gap between current strain and forward-looking confidence, with firms expecting that tighter customer risk management, stronger collections discipline, and operational measures will gradually support performance, even if underlying conditions remain challenging.

When asked about the main risks expected to affect the outlook for B2B payment behaviour in the coming months, companies in India identify a slightly different mix compared with Asia, placing greater emphasis on domestic economic pressure and operational disruption. This focus reflects the reality of a market where payment risk is closely linked to business conditions on the ground. Concern about economic slowdown is more pronounced, reinforcing expectations of continued pressure on cash flow and payment performance. By contrast, inflation concerns are less acute, while views on interest rate risk remain broadly in line with the region.

Operational risks are more prominent in India, with more firms pointing to regulatory changes and supply chain disruptions as key concerns. These factors highlight the importance of managing day-to-day uncertainty in trading conditions. In contrast, cybersecurity risk is cited less frequently than across Asia, suggesting that firms place relatively less emphasis on system related threats and more on commercial and operational challenges. Fraud risk remains broadly consistent across both India and the wider region.

Overall, the risk profile in India is more closely tied to real economy and operational dynamics than to purely financial or systemic factors. This reinforces the liquidity pressures already evident in the market and underlines the importance of active and disciplined customer payment risk management. As the year unfolds, businesses are likely to rely increasingly on early intervention, stronger monitoring, and tighter credit control to navigate a complex environment and protect profitability.

For a full overview of the 2026 survey results for India, please download the market specific report from the related documents section below. Insights into Asia are available in the related content section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.