Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights

Singapore

Singapore

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Singapore

Romania

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Kingdom

United Kingdom

United States

United States

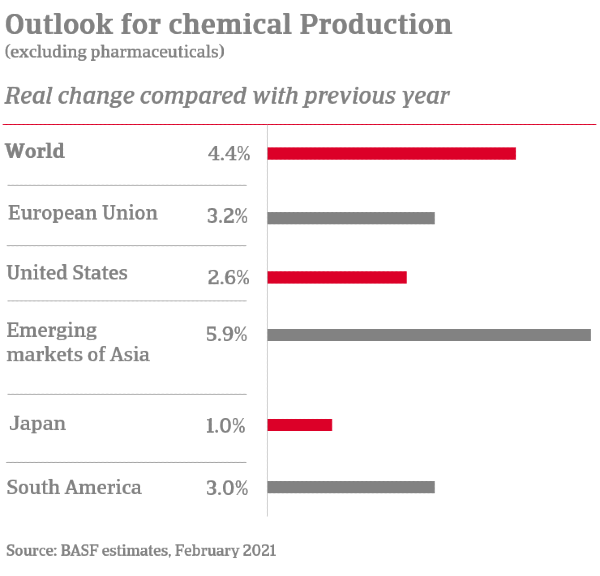

The global outlook for chemical production is positive, with growth projected by most analysts, especially for China and emerging economies. According to BASF, global chemical production (excluding pharmaceuticals) is expected to grow by 4.4% in 2021. This is above average for the years prior to the coronavirus pandemic and represents a strong rebound following the pandemic recession where overall global chemical production contracted by 0.4% in 2020, (compared to an increase of 1.9% in 2019).

4.4% increase in production

The demand for agrochemicals is expected to be the highest in Asia Pacific, where there is a strong agriculture tradition. India, Sri Lanka, China and Vietnam, in particular, are heavily dependent on agriculture and related industries for economic growth. A key trend seen in the agrochemicals segment in recent years is an uptick in M&A activity. The global agrochemical market is witnessing consolidation that is contributing to volume declines in some measures but overall creating some examples of large powerhouses.

This growth is being driven by increasing demand for high-performance and function-specific chemicals. The industrial and institutional cleaners segment accounted for the largest market revenue share of 8.6% in 2019 and is projected to witness a growth rate of 4.0% over the forecast period. The CASE segment that includes coatings, adhesives, sealants and elastomers is also emerging as a potentially lucrative area and accounted for a value share of 3.4% in 2019. Construction chemicals are also expected to emerge as one of the prominent product segments with significant growth projections between 2020 and 2027.

Healthy growth is also predicted for the consumer chemicals sector, particularly within the cosmetics and aroma segments. Asia Pacific is the largest regional market for aroma chemicals. It captured a revenue share of 29.6% in 2019 and most forecasts predict continued market dominance driven largely by the fragrance, food and beverage industries in China, India and Japan. The global aroma chemicals market size was valued at USD 5.5 billion in 2019 and is expected to grow at a compound annual growth rate of 5.8% between 2020 and 2027.

Environmental and social governance (ESG) issues are at a tipping point for the chemicals industry and are impacting businesses across the sectors. This can be seen in both push and pull influences as companies respond to regulatory directives, customer preferences and boardroom guidance. In addition to chemicals regulations in most major markets including the US, Europe and China, there is growing demand among consumers for ‘green’ and ethical products. ESG performance is expected to be benchmarked as highly as cost and other productivity metrics.

The ongoing adoption of technological developments is a feature of the chemicals industry that can be seen in every segment and creates both opportunities and risks. The growing need for process efficiency is driving the adoption of technologies such as IoT (Internet of Things) sensors for both production processes and end product performance. There is also an increasing adoption of blockchain technology to enable supply chain transparency and product traceability around the time-specific delivery of chemicals in end-markets.